2022 in Review: A Sudden Shock of Realism

Amazon opened 2022 with announcements targeting the smart home community that is forming around the Matter protocol and opportunities for IoT in non-residential sectors. These two initiatives are examples of how some large organizations are trying to have a “finger in many pies” to make the most of the variety and scope of IoT opportunities.

2022 closed with a flurry of Matter-compliant product launches from a range of large and small businesses. The year-long journey and commitment to an industry-alliance model point to a degree of realism about the IoT market. Behind the technology fanfare, they highlight how businesses and getting to grips with commercial market-development and the technical challenges associated with interoperability, both of which are needed for scale. Meaningful collaboration seems to be taking hold compared to “go-it-alone” strategies.

Several other corporate developments over the course of 2022 point to a growing sense of commercial and strategic realism. Many of the underlying issues involve individual organizations confronting their lack of market scale. Alternatively, they are dealing with the fact that their offering is either not unique or targets a limited portion of what is required to support a full IoT system. I highlighted the consequences of these supply-side characteristics in my closing comments of 2021. The growing band of IoT adopters require greater awareness of the risks of tying their businesses to a single vendor, a single solution-provider, or a proprietary technology. It seems that several providers grasped the commercial costs and long-term commitments associated with narrow strategies and responded with an exit maneuver.

Multi-strand Strategies

The decision to stay or exit the IoT market is an increasingly real challenge for large and vested players. They can see the large opportunity that IoT enables even if the pathway to large-scale and long-term commercial success is not entirely clear. How do they grasp the opportunities and stain the market for long enough to make solid commercial returns?

Amazon is one organization that is playing on multiple strands spanning connectivity, cloud infrastructure, developers and IoT data. Over the course of 2022, it launched initiatives in support of the Matter protocol and the smart home opportunity. Another initiative involved Amazon Sidewalk which operates a long-range, low-power IoT network using Bluetooth and LoRa radios built into Echo and Ring devices. The network connects devices to Amazon's cloud when they are beyond the reach of traditional homes. To partner with industries and organizations beyond the reach of the current network, Amazon added a new gadget to fill coverage gaps seeking to reach farms, factories and other nonresidential settings. Paralleling its own low-power network service, Amazon Web Services (AWS) entered into a strategic agreement with Semtech for asset tracking and monitoring solutions. The goal is to make Semtech’s LoRa Cloud global navigation satellite system (GNSS) geolocation services accessible to the AWS global developer community. In yet another initiative, AWS is also helping 1NCE to expand the global reach of its IoT platform by co-developing software that speeds up global deployment of IoT projects.

A second large organization is Vodafone. It focuses on cellular connected IoT devices, offering customers a global network supported over its home-grown IoT platform. One of Vodafone’s initiatives was an extension into the farming sector. Its MyFarmWeb service which is used by 7,200 farmers in other continents is being piloted across several European countries. Farmers can use a mobile app linked to agricultural IoT sensors and a cloud-based platform to store, visualize, and view information gathered via IoT sensors and other data sources in the field. They can then make informed decisions about soil and crop health, water use, and the application of fertilizers and pesticides. Vodafone also added to its healthcare sector activities. It partnered with Proximie to ‘digitise operating and diagnostic rooms’ through 5G, IoT and edge computing infrastructure provided by Vodafone Business.

In addition to its vertical sector initiatives, Vodafone seems to be experimenting in other directions to move up the IoT value chain into the new “Economy of Things.” Early in 2022, Vodafone launched a new platform, called Digital Asset Broker (DAB) to help businesses across multiple industry sectors to transform physical goods into tradable digital assets. The service allows verified connected devices, vehicles, smart street furniture and machines to transact seamlessly and securely without human intervention, but with full owner control. Vodafone intends to provide secure links to many other third-party platforms and their associated device eco-systems. This is presumably to create a horizontal capability for cross-silo interactions across industries. It remains to be seen whether this is a form of Blockchain experimentation or a long-term commitment to highly automated, low human-touch data sharing. The recent experience of Maersk, the shipping company, and IBM with their TradeLens offering illustrates the challenges that Vodafone can expect to encounter. The vision for TradeLens was to digitize global supply chains via and open and neutral industry platform. While Maersk and IBM developed a viable platform, they did not secure global industry collaboration which led them to discontinue TradeLens for commercial viability reasons.

Competitiveness, Concentration and Market Exits

The IoT industry’s ever positive narrative of vertical-sector entry and market expansion experienced several major setbacks over 2022 in another sign of growing commercial reality. The long talked about consolidation in the cellular modules sector saw Thales selling its unit to Telit to create a new entity, Telit Cinterion. For relative newcomers to the industry, the M2M modules business was dominated by the likes of Cinterion (acquired by Gemalto and then folded into Thales), Wavecom (acquired by Sierra Wireless) and Telit. Soon after Telit’s gain Semtech, the LoRa proponent, launched discussions to acquire SierraWireless.

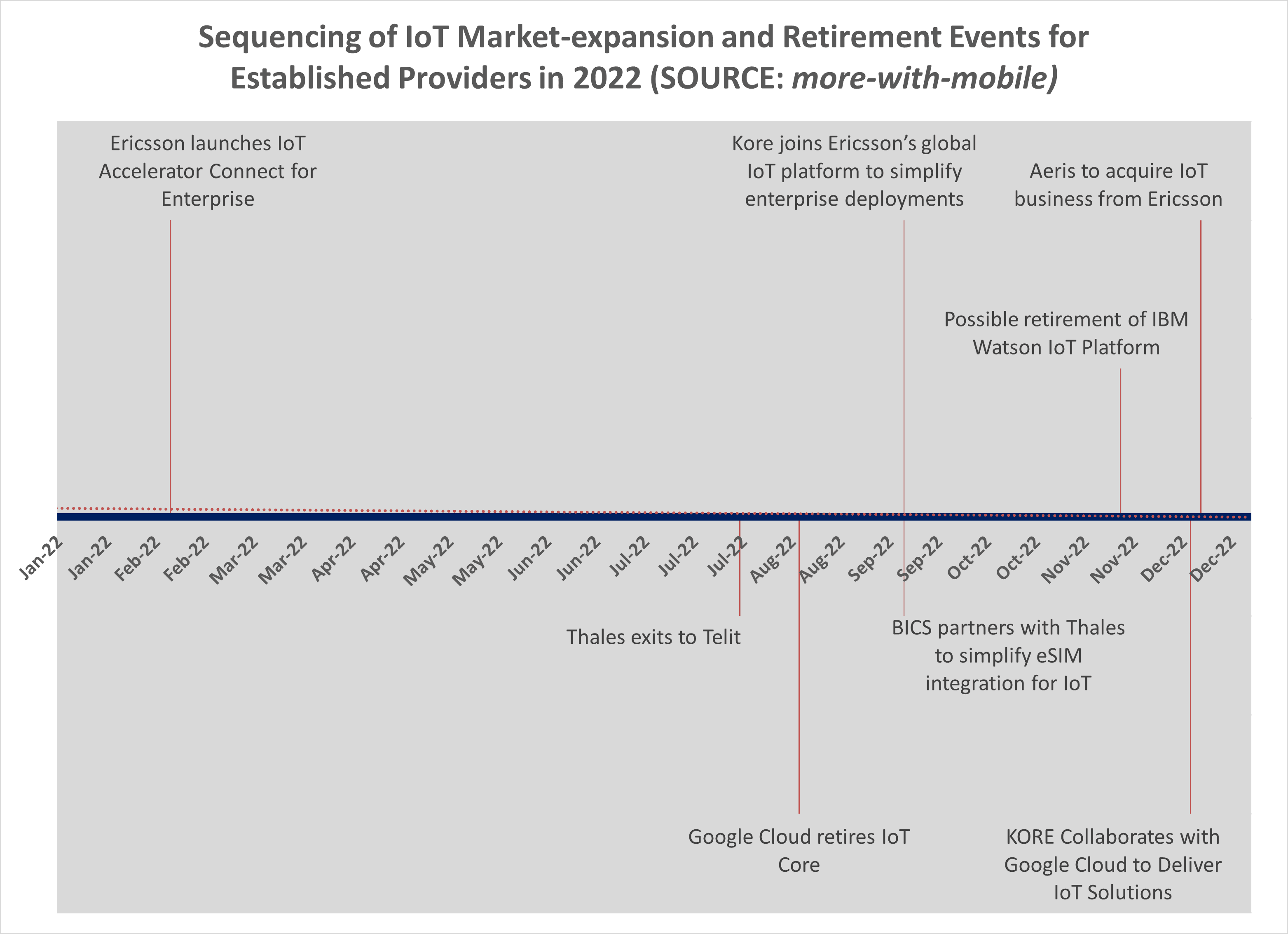

Economies of scale can explain consolidation in the modules market. Two other developments that surprised the IoT industry involved organizations in platform and services parts of the value chain. First came Google’s decision to exit the IoT platform business and withdraw customer support from August 2023. Later in the year, Google’s Cloud unit established a go to market alliance with KORE to provide a rich set of 'one stop shop' services to orchestrate IoT devices, global connectivity, services, data handling and analytics. Google’s initiatives suggest that a withdrawal from the Platform as a Service (PaaS) segment to focus on its strengths as an Infrastructure as a Service (IaaS) provider.

Ericsson’s December decision to transfer its IoT Accelerator and Connected Vehicle Cloud activities to Aeris was a second market surprise. Prior to this announcement, Ericsson’s corporate initiatives suggested continued commitment to the IoT market. In February, it launched IoT Accelerator Connect, a plug and play solution for connectivity, aiming to make IoT connectivity easier than ever for enterprises. During September, KORE joined Ericsson’s IoT Accelerator ecosystem, apparently filling in a North American role that Sprint previously occupied until the latter’s acquisition by T-Mobile USA. Ericsson explained its exit to Aeris by reference to the need for consolidation in a fragmented market and the unsustainable financial losses associated with its IoT business model.

Finally, there is a not fully substantiated story that IBM plans to retire its Watson IoT platform service.

Missed Opportunities and User-led Market Development

Might the realism and shake out of the supply side of the industry be signaling a shift to demand-side initiatives? Attempts to tie users to a particular technology or partner ecosystem might solve narrow use-case opportunities. As systems evolve and new requirements arise, the next stage of development calls for investment in customization or systems integration activities. Difficulties also arise when businesses want to innovate beyond the capabilities and expertise of what one or a small group of providers can offer. This is a throwback to more than a decade when the GSMA launched its market development initiative to expand the M2M market. Still today, organizations complain about fragmentation and complexity.

The IoT market continues to be associated with significant economic value creation. The fact that so many established players – from module makers to platform providers – are exiting this market suggests a missed opportunity, or one where incumbents could not adjust their traditional business models to the characteristics of the IoT sector. The pendulum might be shifting to the demand side of the industry now that IoT technologies are mature and better understood. Specialist users might be taking matters into their own hands as in the case of Siemens acquiring Senseye a specialist IoT solution provider to capitalize on industrial IoT opportunities. For mobile network operators, this dynamic has a parallel with enterprises getting into the business of running private communications networks.

Developments To Watch

The arrival of 5G networks and technology is providing impetus to the market for private mobile networks. 5G is also associated with enhanced mobile broadband (eMBB) and ultra-reliable low latency communications (URLLC) use cases. Now, there is growing activity in the less well addressed area of massive machine type communications (mMTC). Among other research avenues, this takes the form of technologies for low-power devices that communicate intermittently and over long service lives thereby providing the foundation for massive IoT and copious data sets.

Early attention on 6G, other than for technology reasons, is directing industry efforts into geo-political, societal, vertical sector and, environmental needs. The latter few topics are closely intertwined with IoT technologies that enable remote monitoring, data sourcing, analytics and digital twins. Consequently, IoT will not disappear off the agenda of incumbents that exited or scaled back their IoT initiatives. To succeed, however, will call for difficult decisions on interoperability and genuine attempts at long-term partnering.

Overcoming fragmentation and complexity is essential for affordability and market scale. Organizations will also need to adjust their business models, allowing for value to be shared more widely and based on more cost-effective resource accounting and settlement mechanisms. That is a reality borne out of the idea that IoT need not be a zero-sum game.

IMAGE CREDITS: Raj Rana via unsplash.com and more-with-mobile.com

1 Sept 2021 update

ReplyDeleteOperators should follow the move of Singtel, Telefónica and TELUS to invest in IoT connectivity start-ups

https://www.analysysmason.com/iot-disruptor-investments-rdme0